The number of new mortgage agreements for the second quarter of this year has reached the lowest in a decade according to the Bank of England.

The last time figures were anywhere near this low was in the first quarter of 2010.

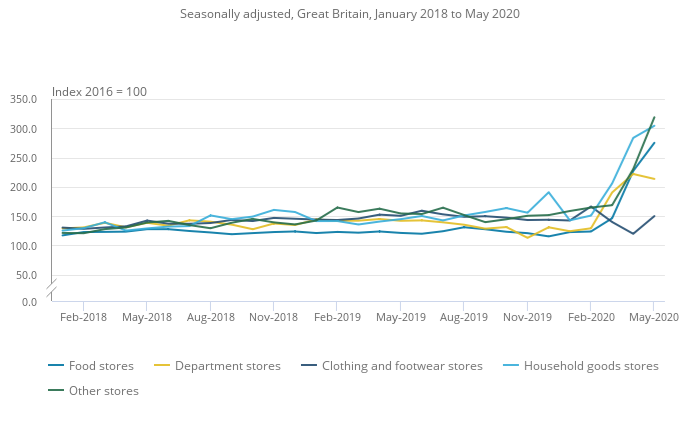

It’s hardly surprising, given property sales had ground to a virtual halt during the lockdown. Much of that had taken place during this second quarter, spanning April to June.

I suspect that thanks to the booming property market, bolstered by a mixture of pent up demand and the stand duty holiday, we’ll see a swift reversal of that in the third quarter of this year, covering July to September.

But while house sales are on the up, the mortgage market remains in a state of flux.

After taking a financial hit from mortgage payment holidays, contending with the persistently low interest rates, and working with the gloomy outlook for the economy, lenders are understandably more cautious.

That’s why we’ve seen furloughed workers’ mortgage applications being rejected outright, high loan-to-value mortgages being withdrawn from the market and more expensive mortgages creeping in.

Some lenders have also started adjusting the amount of money they are willing to lend.

For example, Barclays would previously have allowed applicants to borrow up to 5.5 times their salary. In recent weeks, this has been quietly adjusted down to 4.49 times of their salary to fall in line with most other lenders.

Natwest has made similar adjustments, reducing the amount they’re willing to lend from 4.9 times of salary to 4.25 times of salary specifically for self-employed workers.

All of this means it’s getting harder to get mortgages, the ones borrowers are able to get will become more expensive and at some point this will bite into the property market.

What it means for you…

It’s not impossible to get mortgages of course – it’s in the banks’ interest to lend money because that’s part of how they make money. But it is getting harder.

While you can absolutely find mortgages yourself using comparison sites or by going direct, employing the services of a good mortgage broker is now more useful than ever.

They can tell you what’s out there, what you might be able to successfully borrow and reduce some of the hassles of searching and applying.

This is especially true when lenders are starting to issue limited time and limited number mortgages for those who only have 10% deposit.

Most mortgage advisors work on a commission basis so you don’t have to pay them more, but make sure you go to one that’s happy to answer all your questions, regardless of how trivial, and will show you everything on the market.