How getting debt advice works

Money Talk is intended to inform and educate; it's not financial advice. Affiliate links, including from Amazon, are used to help fund the site. If you make a purchase via a link marked with an *, Money Talk might receive a commission at no cost to you. Find out more here.

Debt is on the rise and all of us are affected in some ways, whether directly or not.

But while some debts can be considered beneficial – for example, a mortgage or a student loan – many can easily turn toxic.

I often signpost to debt charities when writing about problem debt, but what happens when you actually contact one for help or debt advice?

To find out, I spoke to Sara Williams, who has been a debt adviser for over 20 years and writes Debt Camel.

What happens when you approach a debt charity for help?

“Most of the debt charity websites have this form to fill in, which basically lists your debts, your income and your expenses in a month,” says Williams. “That is the starting point for debt advice.”

The forms are designed to help you build an accurate picture of your finances. And once you have that, you can then work out what your disposable income is.

“The aim of debt advice is to use your disposable income to pay off your debts as soon as possible,” says Williams.

How to work out your disposable income

Your disposable income is basically your income minus any expenses and payments to your priority debts.

Expenses might include things like food, clothes, toiletries and a bit set aside for Christmas while priority debts are the things that you have to keep paying, says Williams.

So that includes things like council tax, energy bills, and car financing, if you need a vehicle to get to work or drive your kids to school.

What options are available when you’re in debt

Depending on how much money you’ve got and how big the debts are, you’ll be given different options for what happens next.

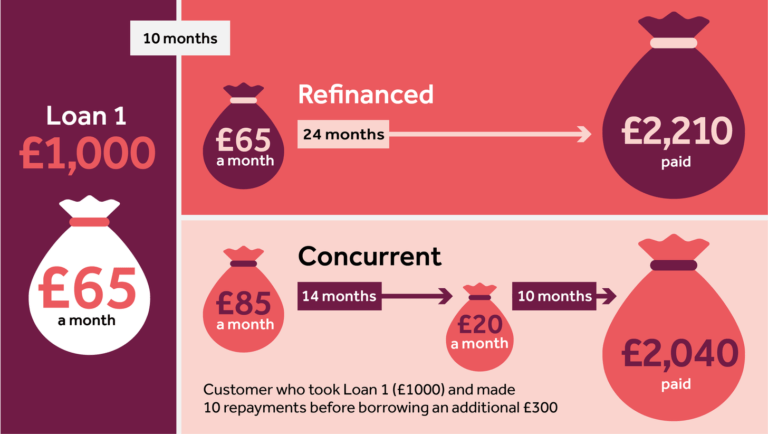

While most people automatically think about debt restructuring, such as consolidating all your debts into a single, slightly cheaper loan or a 0% credit card, this may not be a good option for a lot of people.

“It might be cheaper than what you’ve got, but it might still be more expensive than what you can afford,” says Williams.

This is especially true at a time when prices are rapidly increasing.

An alternative option might be a Debt Management Plan (DMP), where you make a single payment to a charity, who then redistributes that money to your creditors.

While you’re on a DMP, which could last for years, all your interest payments are frozen so you can just focus on paying off your debt.

And if a DMP doesn’t work, you may end up going into insolvency.

How long does the process take?

“How long it takes depends on how complicated this is for you,” says Williams.

If you just have a couple of credit card bills, the process might be pretty straightforward. But if you’re self employed and have business debts, or you live in a mixed household, things might be a bit more complicated.

Once you fill in the form, you’ll get put through to a debt adviser who’ll talk you through your form, and then you can amend any details or make additions if you’ve forgotten something.

Getting an appointment can take a week or two, especially if you’re trying to make an appointment first thing on a Monday because you’ve been thinking about it all weekend, or at lunchtime.

The trick is just to persevere, says Williams.

And then depending on what options may be best for you, it can take up to a month or two to get things in place for a debt management plan – although the process starts straight away – or around an hour to declare bankruptcy.

Do you need to do any preparation?

Although you don’t need to, any preparation you do will make you the debt adviser’s favourite client, says Williams, and make the process of getting debt advice much easier.

When you fill in the form, it’s best to be as detailed as possible, although you will have a chance to amend it later on.

Many people don’t paint a very accurate picture of their finances.

Often, it’s because people haven’t budgeted in detail, so they just don’t know the exact number and will “just pluck a figure out of the air”, says Williams.

You might also omit things that you don’t pay for every month.

Williams said: “It’s common to see nothing on there for dentists or opticians, nothing on there for haircuts, or gifts if you’re nowhere near Christmas.”

She added: “Things that you know you’re going to spend money on throughout the year, you need to allow a certain amount each month. Otherwise, you won’t have a realistic picture of your overall expenses.”

It’s also good to look at your bank and credit card statements because then you can identify anything that you can get rid of straight away.

“Subscriptions are the classic example,” says Williams. “Just chop those out and you don’t need to bother to think about them anymore, and that’s money saved.”

Finally, Williams recommends writing down the questions you want to ask because it’s easy to forget something when you’re on the phone.

Read this: How to manage spending and save money

Is there anything you should be aware of?

Some debt solutions can affect your credit score.

And things that affect your credit score will also affect your ability to get certain types of insurance, according to Williams – although this tends to be on policies where you’re paying on a monthly rather than an annual basis.

You’ll also find it harder to remortgage, or get a mortgage in the first place.

And unfortunately in some cases, there’s no way to get around it if you want to get out of debt.

“You have to be realistic about this,” says Williams.

“You might want to buy a house in three years’ time, but if you’ve got problem debts at the moment, it’s not going to happen. You can’t save up money for a deposit when you’ve got debts you’re trying to manage.”

Why it’s important to sort out your debt anyway

“The only way you’re going to get through to owning a house some time in the next five to 10 years is if you take control of your debts now,” says Williams.

“Otherwise, you’re just going to be there in three years’ time still thinking, ‘well, I’ve still got these debts, I haven’t really managed to save up for a deposit, and I haven’t made any progress.’

“At least in three years’ time, if you say ‘well actually I’ve now paid off three quarters of my debts in the debt management plan’, you’ve got a timescale and you know what you can afford.

“So don’t let a fantasy about owning a house in the future stop you from taking control of the situation at the moment.”

For those who already have a fixed rate mortgage in place that’s coming to an end, you’re unlikely to get a new offer from another lender if your credit score is awful.

However, you can normally get a new one with your existing lender regardless of your credit score.

The good news is that your credit score is something you can rebuild over time, and it’s much easier to do this when you’re not in debt.

And it’s much better to take control early on, when you have different options, than go into a debt spiral and find out further down the line that you can’t borrow any more to fix your problems.

Pin this for later