Take care if you’re refinancing debt

Money Talk is intended to inform and educate; it's not financial advice. Affiliate links, including from Amazon, are used to help fund the site. If you make a purchase via a link marked with an *, Money Talk might receive a commission at no cost to you. Find out more here.

The Financial Conduct Authority (FCA) has released a new report on the practices of high cost lenders and it’s really eye opening.

A lot of the case studies they’ve included were stories of how people ended up in debt cycles because of the high interest rates.

That bit is not really surprising.

What is surprising is how consolidating a loan – or refinancing debt as it is sometimes known – can actually get people into further debt.

For me this is a particular point of interest because a lot of the narrative around debt encourages people to consolidate their debt, because it will make repayment more manageable and affordable.

And it does – but it could also increase their debt burden in the long run.

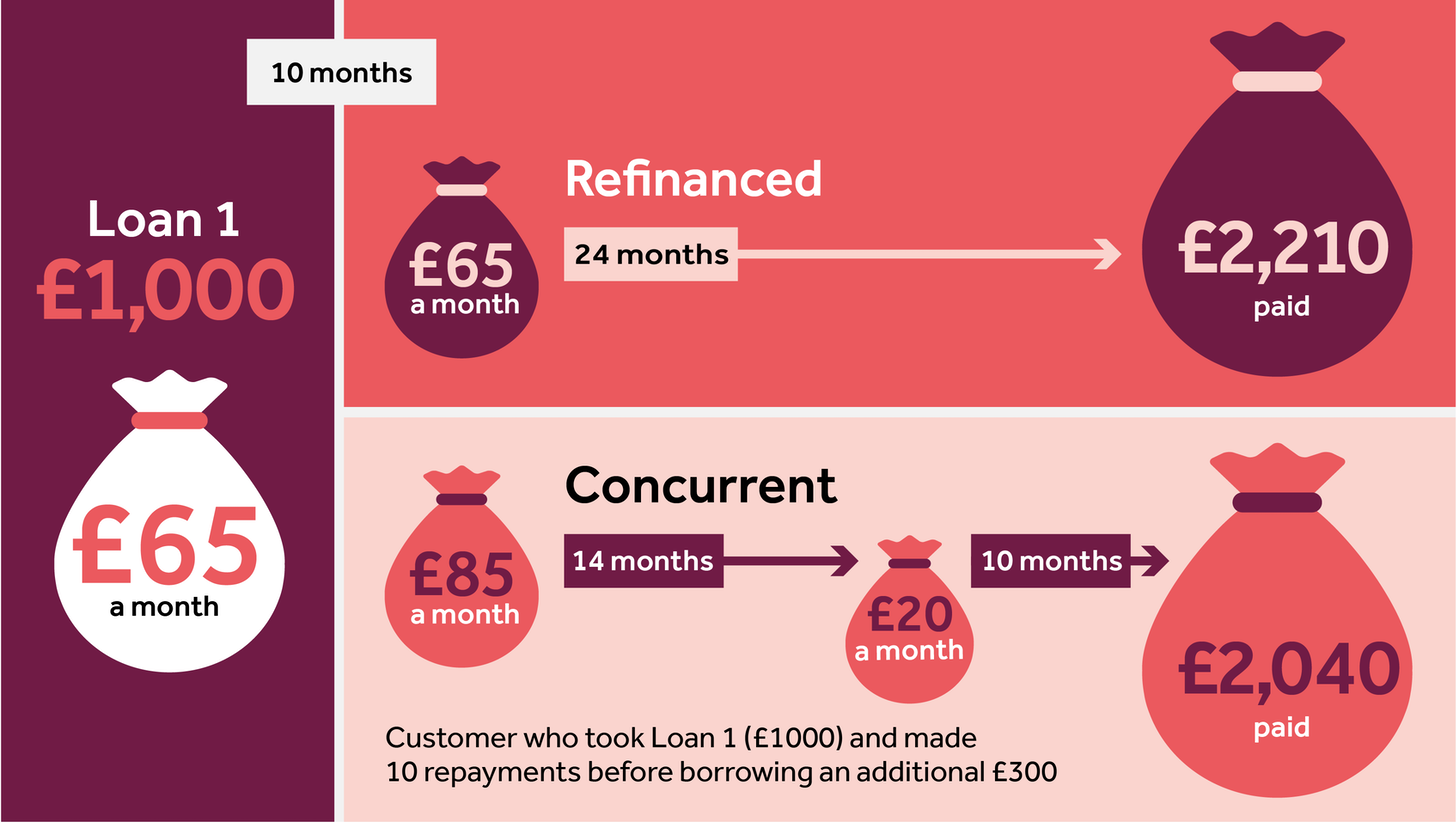

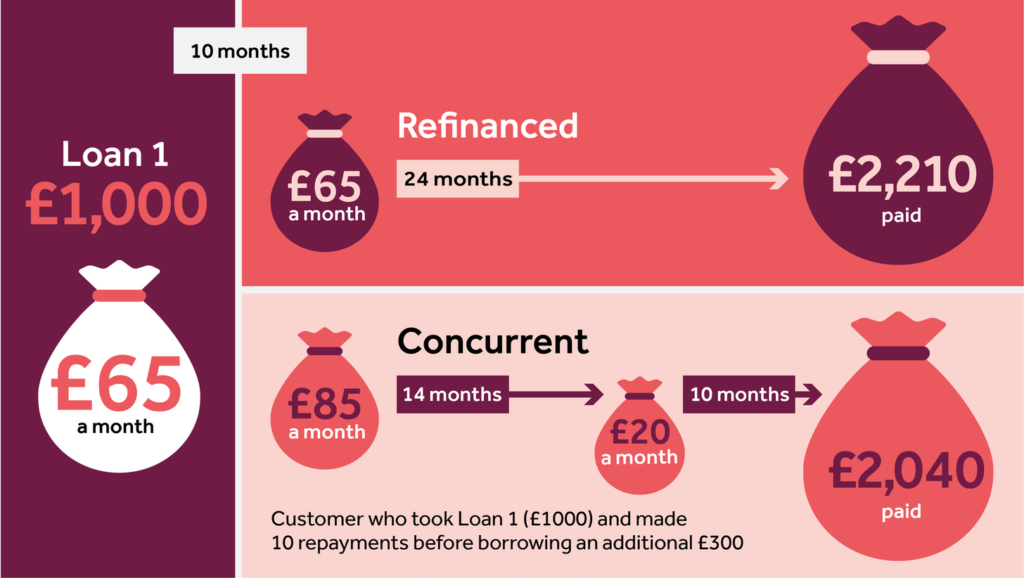

The example the FCA used was someone who took out a loan for £1,000 and was repaying it at a rate of £65 a month. After 10 months, they borrowed an additional £300.

But because of the interest rate and length of time it takes to pay back a refinanced loan, it actually costs more overall than having two concurrent loans (two separate loans that you’re paying back at the same time).

This example certainly demonstrates why you should double check what you’re paying.

Of course, the repayment rate for concurrent loans is higher per month, and not everyone can afford this, but those who can will miss out if they don’t check.

If you are in debt, get some professional advice. There are a few debt charities around that can help, including Step Change.

Read more: How getting help from a debt charity works