UK GDP has dropped off a cliff

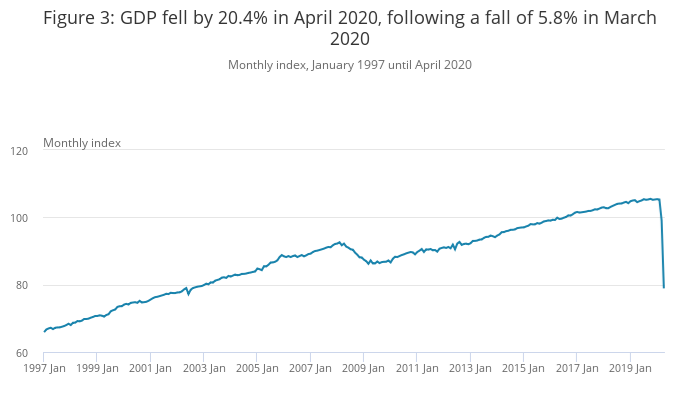

The Office for National Statistics (ONS) has just released April’s GDP estimate for the UK and it’s taken a 20.4% dive.

Plotted against historical data, it looks like we’ve plunged off a cliff.

And according to Jonathan Athow, deputy national statistician for economic statistics, “April’s fall in GDP is the biggest the UK has ever seen, more than three times larger than last month and almost ten times larger than the steepest pre-covid-19 fall.”

This means the UK’s GDP has dropped to just below August 2002 levels. We have fallen even further than the years just after the 2008 financial crisis.

Your warning bells are probably ringing. Mine are. But don’t panic just yet.

To put this in context, here’s how GDP is calculated

GDP, or gross domestic product, can be calculated using one of three approaches:

- Production: this is the market value of goods and services that are produced eg how much I charge for this newsletter.

- Income: this is the money that is generated through the sales of goods and services eg what I receive from your paid subscriptions.

- Expenditure: this is the amount of money spent on good and services eg what you pay for these subscriptions.

In theory, all three approaches can be used because they’re all interchangeable. Production feeds into income, which in turn feeds into expenditure; and expenditure then fuels the production, creating a cycle.

It’s worth taking the results of April’s GDP estimates with a pinch of salt for several reasons.

Coronavirus lockdown has imposed significant limitations on how data used to calculate GDP is collected, or indeed whether it can be collected at all. So right now, GDP estimates are not at their most accurate.

In addition, month-on-month GDP estimates are inherently much more prone to fluctuations than quarterly ones.

What is clear is that the situation right now is bad. In the three months leading up to April, GDP had already fallen by 10.4%.

It’s led by service industries such as travel and hospitality, but international trade has also had an impact.

April is looking particularly glum because of the lockdown – many sectors of the economy were forced to shut down. We’ll see this reflected in May’s GDP estimates (due to be released on 14 July) as well as in June.

With this in mind, we can assume that as lockdown eases across the UK over the coming months, all of those sectors will bounce back. GDP won’t, and it can’t, return to pre-Covid levels for the foreseeable future, but it won’t be in such dire straits either.

What it means for you…

Clearly we’re in for some tough times, not least because Brexit is happening in just over six months.

The proposal of a €500bn Europe recovery fund by France and Germany last month is a stark reminder of how we won’t have that support anymore.

As individuals, we can still look ahead.

Now is the time to consolidate debt for example.

You should also think about creating an emergency fund. Experts generally say to save enough for three to six months of living expenses (rent, food, bills and extras), but for now, I would prepare for up to a year as a buffer.

Even if you’re in a steady job, it’s worth thinking about other income streams. That might mean a side hustle, but it could also mean looking into investments. Be cautious with the latter – we’re in for a long dip before things pick up in earnest.

And if you have kids, you’ll have to think even further ahead. The effects of coronavirus isn’t just short term, it could be generational according to the Institute for Fiscal Studies.