Accumulation or income fund: Which is better?

Money Talk is intended to inform and educate; it's not financial advice. Affiliate links, including from Amazon, are used to help fund the site. If you make a purchase via a link marked with an *, Money Talk might receive a commission at no cost to you. Find out more here.

You’ll often see the same fund listed twice on investment platforms; one is labelled accumulation and the other is labelled income.

While their names and investment outlooks might look largely similar, whether you should choose an accumulation or income fund will depend entirely on your circumstances.

This can include how long you plan to stay invested and what platform you’re using, but also how much you have invested and what kind of investment wrapper you’re using.

It doesn’t have to be an either/or situation though – sometimes a combination of the two can work in your favour.

Either way, understanding the mechanics of the two types of funds will help you decide what’s right for you.

What are accumulation and income funds?

Regardless of whether you’re investing in an index fund or an exchange-traded fund (ETF), most funds come in two versions.

One version is the accumulation fund, where any profit earned is reinvested into the fund rather than paid out as a dividend.

The other version is the distribution fund, which is generally labelled as an income fund.

As its name suggests, any profit earned in an income fund is distributed as dividends, which many people use as income.

When to choose an accumulation fund

Accumulation funds are designed for those who intend to stay invested for longer periods of time (we’re talking decades here) and don’t need dividends as a source of income.

The reason is that instead of paying you dividends, the fund reinvests its profits with the goal of adding value to every single unit in the fund.

With any luck, in several decades’ time, the value of each unit will have grown such that when you come to sell your investments, the difference between what you bought the units for and what you’re selling them for will net you a tidy profit.

The main takeaway here is that you’ll only profit from your accumulation fund investment when you sell it.

As with any type of investing, there’s no guarantee that your investments will have grown in value or have grown enough to net you a profit.

You might even make a loss if you’re forced to sell your holding during a downturn in the market.

When to choose an income fund

A distribution or income fund is best for those who want a regular income from their investments.

This typically means someone who is retired, and relies on the dividends for income, though not always (more below).

Unlike accumulation funds, income funds will pay dividends to investors on a quarterly, six monthly or annual basis.

You can withdraw that money to use as income or you can manually reinvest the money.

The value of each unit of the income fund will also increase over time, though at a slower rate compared to an accumulation fund.

That means if you decide to sell your income fund further down the line, you might receive a profit in addition to the income you’ve received over the years.

Again, as with any type of investing, a return is not guaranteed.

The fund might have performed particularly poorly and therefore you’ll receive little to no income at all.

What about risk?

You may well be thinking that an accumulation fund sounds more risky than an income fund.

After all, you can at least hope for some regular income with your income fund alongside investment appreciation, whereas an accumulation fund feels more like an eggs in one basket situation.

But the risk profiles of the two different types of funds extend deeper than that.

Even though the accumulation and income fund might fall under the same overarching fund name, what they invest in can be very different.

Accumulation funds might have a bigger emphasis on growth-focused assets in their portfolio, such as stocks with high potential for capital appreciation, which can be slightly riskier.

In contrast, income funds might focus more on income-generating assets, such as dividend-paying stocks, bonds, or real estate investment trusts (REITs), which might be less risky.

But to properly determine risk, you’ll have to drill down into each version of each fund, which can be quite time consuming.

This is where a financial adviser specialising in investments can come in handy – assuming you have a decent sized portfolio to invest.

Accumulation vs income fund: Which is better?

As I wrote earlier, whether you should choose an accumulation fund or an income fund will depend on your circumstances.

Sometimes it doesn’t matter which one you choose and sometimes it matters a lot.

And sometimes it can be beneficial to hold a combination of the two funds.

Below isn’t an exhaustive list of things to consider, but it’s a good starting point.

Time under investment

Investing is a long game.

Experts often recommend that your money stays invested for at least five years, but it can be much longer before you see a real difference in the size of your portfolio.

If you’re only planning to stay invested for a short period of time – so less than five years – the chances are you’ll see very little difference in how much the two versions of the same fund will have grown, even if you don’t manually reinvest the income.

The only things that might make a difference are the fees you’re paying (more below) and how much you have invested.

But if you’re planning to hold the same fund for several decades, and you’re not reinvesting the money, which fund you hold will make a big difference.

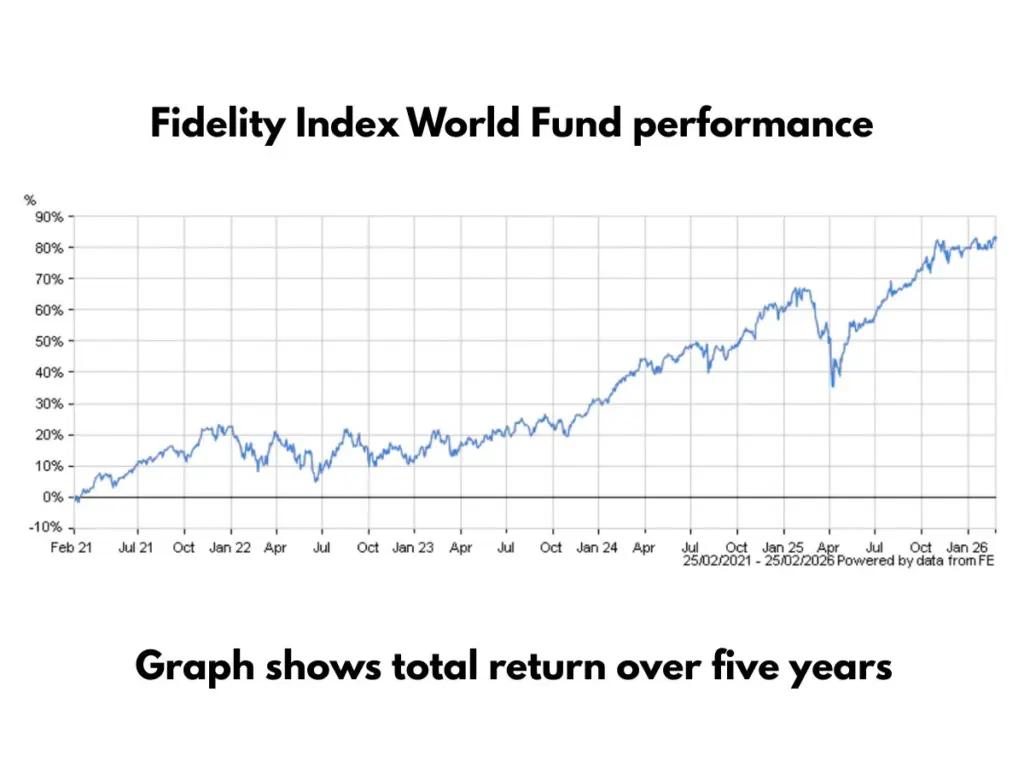

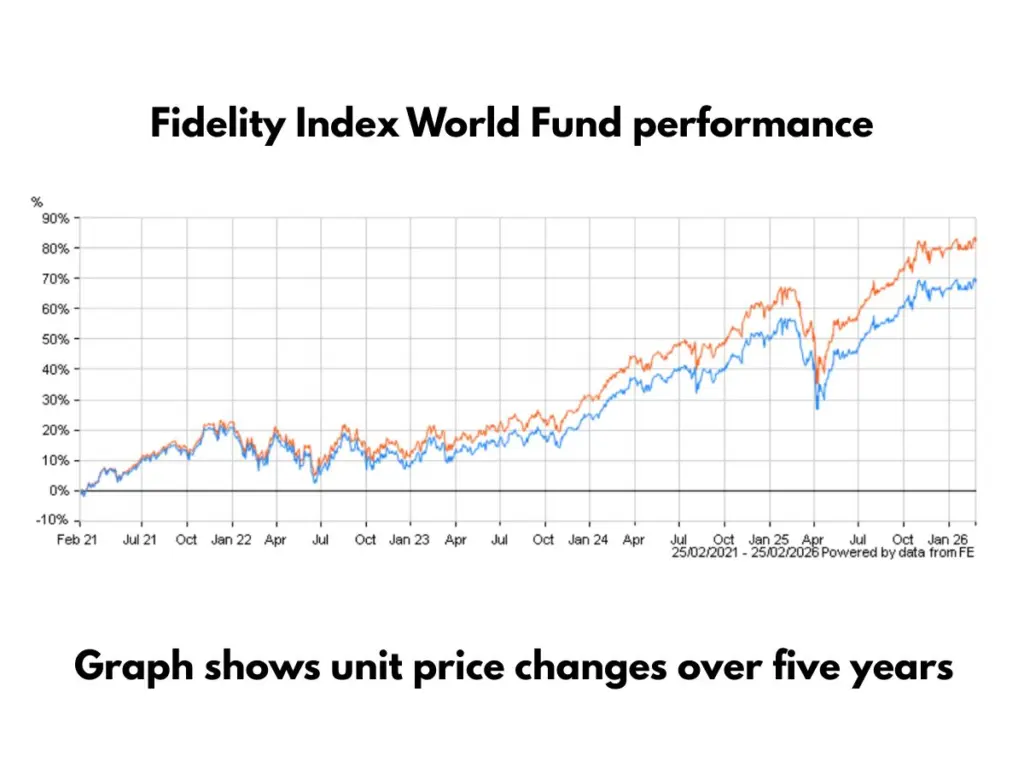

Let me use the Fidelity Index World Fund as an example because it’s one of the funds I hold. The numbers below are for February 2026.

On Hargreaves Lansdown’s website* you can compare the accumulation and income versions of the same fund, and see both the total return and the unit price.

When you look at the total return (fund unit price plus reinvested dividends), the difference in value between the accumulation and income versions of the fund are negligible over a period of five years.

That is, if you reinvest your dividends, you won’t see much of a difference in the value of your portfolio after five years regardless of whether you’re holding accumulation funds or income funds.

However, when you look at the price per unit, the accumulation fund is growing at a much faster pace than the income fund over the same five year period.

After a year, the accumulation fund unit price has grown 12.9% while the income fund unit price has grown 11.35% – that’s a difference of 1.55%, which isn’t a huge amount.

But after five years, the accumulation fund has grown 83.38% while the income fund has grown 69.85% – now it’s a difference of 13.53%.

Put crudely, that’s the growth you’re losing in just five years on this fund if you don’t reinvest those dividends.

Amount invested

The amount of money you’ve invested will make a big difference if you’re not planning to reinvest the dividends.

Let’s say you bought £1,000 worth of those Fidelity Index World Fund units.

Based on the figures above, after a year your portfolio will have grown to £1,129 in an accumulation fund, and be worth £1,113.50 in an income fund, assuming dividends are not reinvested.

That’s a difference of £15.50, which is not a huge amount.

But if you had £10,000 invested, that difference becomes £155; or if it’s £100,000 invested then it’s a sizable £1,550.

Tangential to this point is how much money you have to invest.

If the answer is not a lot, and you want to experiment with different funds before you find the right one, an income fund can free up a bit of extra cash in dividends as it grows, which you can then reinvest in a different fund.

Stage in life

For those who are retired, income funds make sense.

Your portfolio will still grow but you’ll also get income from your investments without having to sell any of it.

But if you’ve retired early, say in your 50s, 40s or even earlier, you might reasonably expect to live quite a bit longer.

In this case you might want to hold a portion of your investments in an accumulation fund and another in an income fund so you can benefit from both.

The investment platform

The investment platform you use can shape how you structure your investments, too.

Most investment platforms will charge a fee every time you make a trade.

Because of this, it doesn’t make sense to manually reinvest dividends from an income fund.

You’re better off picking an accumulation fund that will automatically reinvest for you to avoid those additional trading charges.

How your investment platform deducts its fees matters, too.

For example, Hargreaves Lansdown takes all fees directly from your investment account.

If you don’t have a cash reserve to cover the fees, it’ll sell some of your investments.

If you have a general investment account where you can add money whenever it’s needed then you could hold accumulation funds and just make additional deposits to cover the fees.

However, if you have an ISA or LISA, where there’s a cap on how much money you can put in, you might end up selling some of your investments to cover the fees if you haven’t left a cash buffer.

The solution may be to hold a proportion of income funds to cover the fees and hold the rest as accumulation funds.

Your investment product

If your investment is held in a tax-free wrapper like an ISA, Lifetime ISA, SIPP or other type of pension, then you don’t need to worry about the tax implications of the fund you choose.

However, if you have a general investment account, that money is subject to tax.

Both income funds and accumulation funds are subject to capital gains tax when they’re sold and you make a profit.

In addition, dividend payments you receive from an income fund will also be subject to income tax.

So if you have a general investment account, it makes much more sense to choose an accumulation fund to lower your tax burden.

Pin this for later